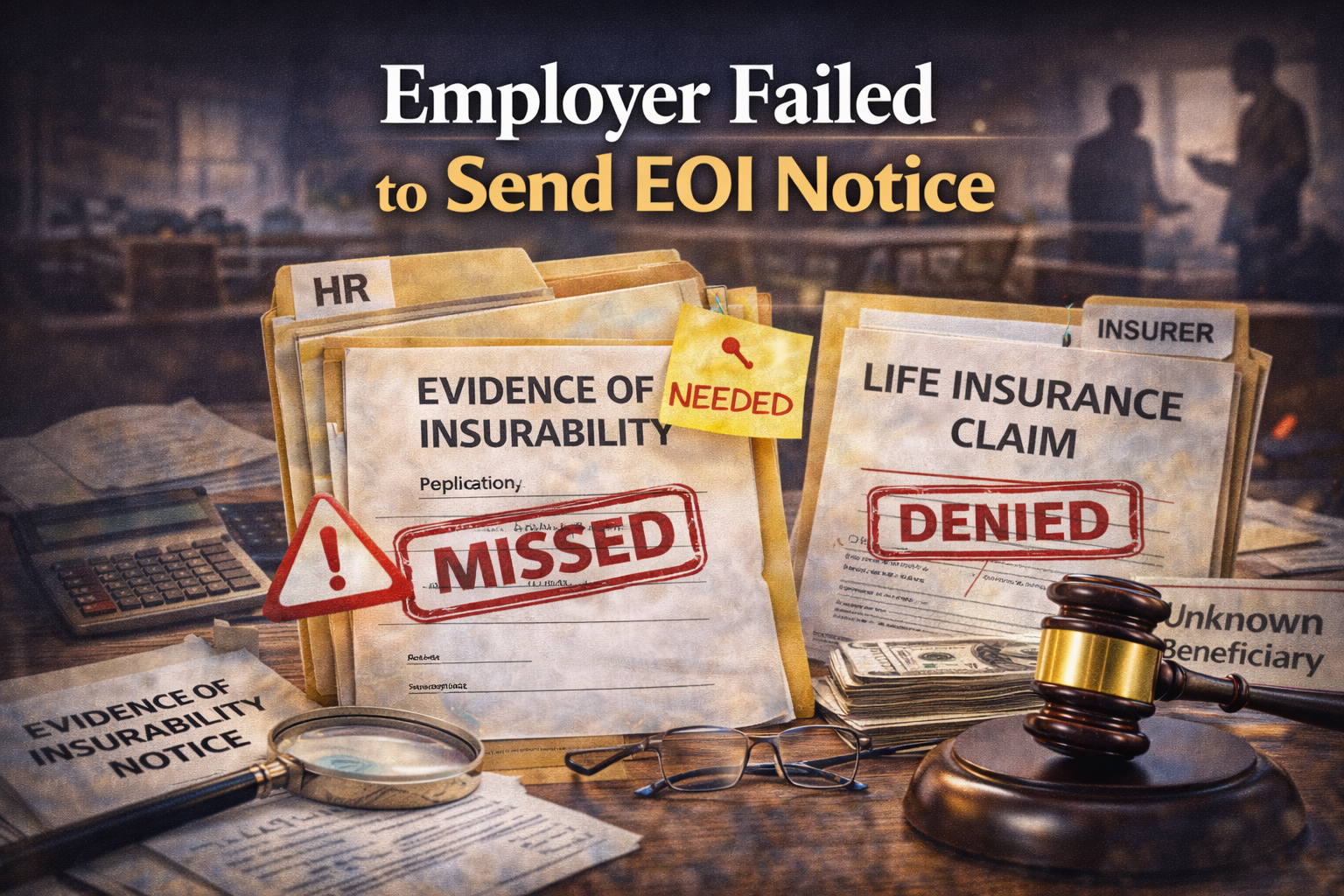

One of the most common employer driven life insurance denials happens when an employee elects supplemental coverage but never receives the required Evidence of Insurability follow up. The employee believes the coverage is active. Premiums are deducted. Enrollment confirmations show the higher amount. HR systems display the coverage as approved. Then the employee dies and the insurer denies the claim because the EOI was never completed.

This is not an employee mistake. It is an employer failure. When employers do not notify employees that EOI is required or fail to send the follow up request, the employee loses coverage without ever knowing it. Insurers then deny the claim and point to the missing EOI. Employers blame the insurer or the system. Families are left with nothing.

How EOI Requirements Work and Why They Are Missed

Supplemental life insurance often requires EOI when coverage exceeds a guaranteed issue amount. The process is simple in theory. The employee elects coverage. The employer or insurer sends an EOI request. The employee completes it. The insurer approves or denies the increase.

In practice, the process breaks down because of employer errors such as:

HR never sends the EOI request to the employee

The employer assumes the insurer will contact the employee directly

The EOI email goes to an inactive or incorrect address

The employer fails to monitor pending EOI cases

The benefits system marks coverage as approved even though EOI is missing

The employer does not follow up when the employee does not respond

These failures create the illusion of coverage. The employee believes everything is complete because premiums are deducted and the benefits portal shows the higher amount.

Why Insurers Deny Claims When EOI Is Missing

Insurers rely on their own approval records. If they never received EOI, they treat the supplemental coverage as never in force. They do not consider payroll deductions. They do not consider enrollment confirmations. They do not consider employer mistakes. They simply deny the claim and pay only the guaranteed issue amount.

Insurers often take the following positions:

The employee never completed EOI

The insurer never approved the increased coverage

The employer had no authority to show the higher amount as active

Premium deductions do not create coverage

The insurer cannot retroactively approve EOI after death

These positions ignore the fact that the employee was never told that EOI was required or that the process was incomplete.

Why Employers Are Responsible for EOI Notification Failures

Employers are responsible for administering group benefits correctly. When they allow employees to elect supplemental coverage, they must notify them of any EOI requirements. They must send the follow up request. They must track pending EOI cases. They must correct system errors that show unapproved coverage as active.

Courts consistently hold employers liable when:

The employee was never told EOI was required

The employer failed to send the EOI request

The employer deducted premiums for unapproved coverage

The benefits system showed the higher coverage as active

The employer failed to follow its own procedures

Employers cannot shift responsibility to the insurer. They cannot claim the employee should have known. They cannot rely on system errors to defeat coverage.

How These Cases Turn Into Multi Party Disputes

When EOI is missing, insurers often deny the claim outright. In some cases, they file an interpleader if multiple beneficiaries are involved. The employer then becomes the primary defendant because the denial was caused by its failure to notify the employee.

These disputes often involve:

Enrollment records showing the higher coverage

Payroll deductions for the increased amount

System logs showing EOI was never triggered

Emails or notices that were never sent

Evidence that HR knew of the missing EOI but did nothing

The case becomes a question of who caused the failure and who must pay.

What Beneficiaries Should Do When EOI Notification Is Missing

Beneficiaries should gather evidence immediately, including:

Pay stubs showing deductions

Enrollment confirmations

Benefits portal screenshots

HR communications

The full claim file from the insurer

Any system generated notices or logs

The goal is to show that the employee elected coverage, paid for it, and was never told that EOI was required.

Why These Cases Require Immediate Legal Action

EOI notification failures are among the strongest employer liability cases in life insurance litigation. The employee did everything required. The employer failed to follow through. The insurer denied the claim. Without legal intervention, families risk losing the benefit entirely.

A lawyer can force the employer to produce internal records, uncover system failures, and hold both the employer and insurer accountable. The focus is always on proving that the employee relied on the employer’s representations and that the employer’s failure should not defeat coverage.