Life insurance companies increasingly rely on digital platforms, online portals, and electronic forms to manage beneficiary changes. While these systems are marketed as faster and more convenient, they have introduced new risks that families rarely anticipate. When a beneficiary change is made electronically, insurers frequently scrutinize the submission and may challenge the signature, the authenticity of the update, or whether the form complied with policy requirements.

These challenges often lead to delayed payments, interpleader lawsuits, or outright denial of the intended beneficiary. Understanding how digital signatures and electronic forms create disputes is critical when a life insurance claim becomes contested. When you are facing a beneficiary dispute, we are here for you. Look at our beneficiary dispute fact sheet for more information.

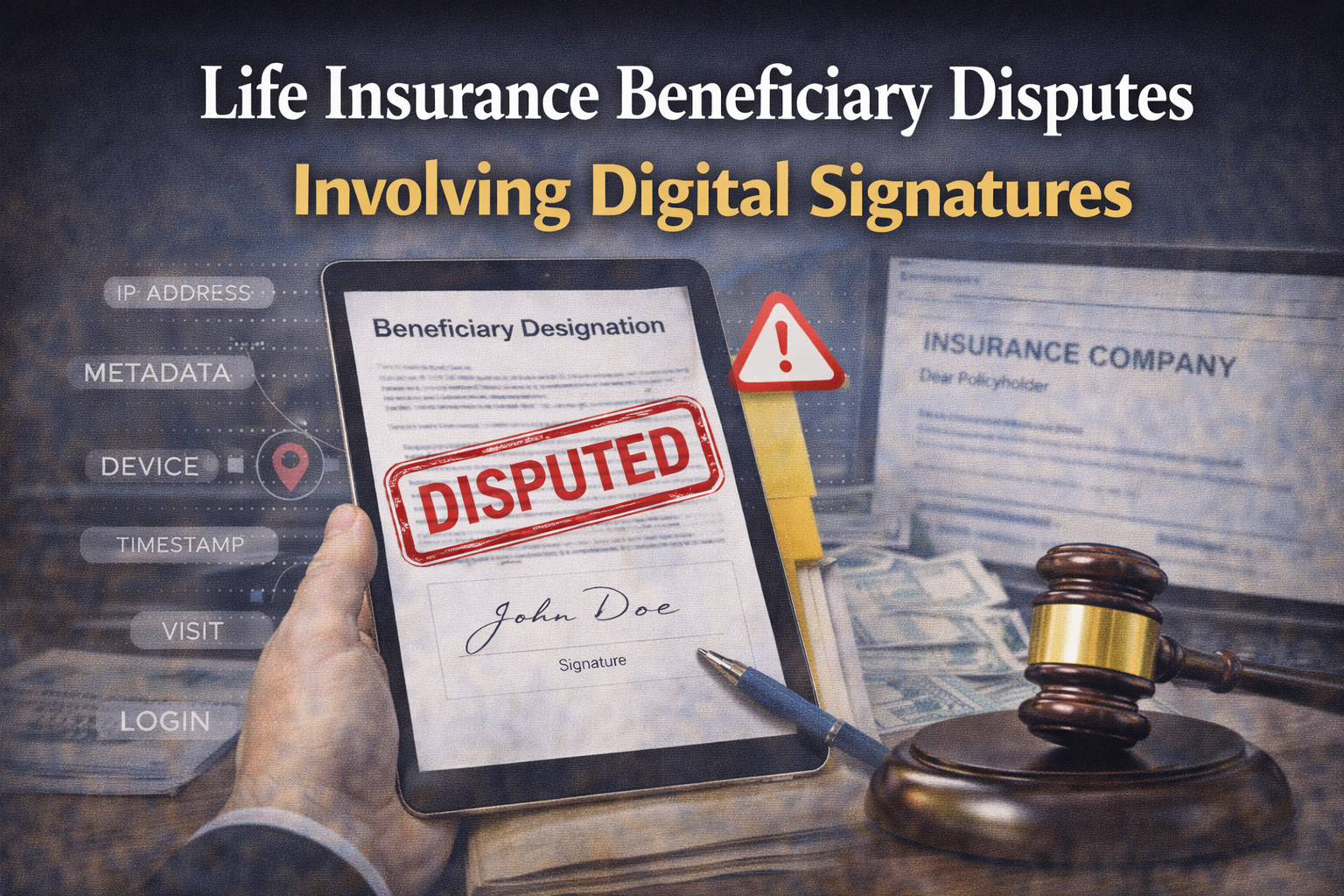

Why Digital Beneficiary Changes Are Frequently Challenged

Electronic signatures are legally valid in most circumstances, but insurers continue to treat them with skepticism. Digital processing introduces technical checkpoints that insurers use to question whether a beneficiary change should be honored.

Common reasons insurers dispute digital beneficiary updates include claims that the signature was typed instead of handwritten, the form was incomplete, or the submission did not match expected user data. Insurers may also point to system failures, outdated software, or assert that the form was never properly received or saved.

When these issues arise, insurers often default to the prior beneficiary designation, even when evidence suggests the policyholder intended to make a valid change.

How Metadata Is Used in Beneficiary Disputes

Every electronic submission generates metadata, which insurers increasingly rely on as evidence. Metadata can include the IP address, device type, time and date of submission, login credentials, portal activity logs, and email confirmations.

If the metadata does not align with what the insurer expects, the insurer may argue that the submission was unauthorized, fraudulent, or unreliable. Even minor discrepancies can trigger extended investigations or lead the insurer to file an interpleader action rather than pay the claim.

Claims That a Digital Signature Is Invalid

Insurers sometimes argue that a digital signature fails to meet policy requirements. They may claim the signature was not properly authenticated, that required verification steps were missing, or that the platform used did not meet internal security standards.

In some cases, insurers assert that the policyholder did not personally complete the form or that someone else submitted the update using the policyholder’s account. These arguments are often used to disregard the digital change and rely on an older beneficiary designation.

Substantial Compliance and Electronic Beneficiary Changes

Courts increasingly recognize that electronic beneficiary changes should be treated similarly to paper forms when the policyholder’s intent is clear. Under the substantial compliance doctrine, a change may be enforced even if technical requirements were not perfectly satisfied.

Substantial compliance may apply when the digital signature was typed, the submission was made through an employer portal, the insurer claims the form was incomplete, or the insurer’s system failed to save the update. If the policyholder took reasonable steps to complete the change, courts may honor the new designation despite administrative or technical flaws.

Fraud Allegations Involving Digital Submissions

Digital beneficiary changes often trigger fraud allegations, particularly when the change occurs close to death. Insurers may question whether someone else accessed the account, whether the policyholder had capacity at the time, or whether a caregiver or family member exerted influence.

Insurers may also focus on whether the device used belonged to the policyholder or whether the login activity appears unusual. These allegations frequently delay payment and increase the likelihood of interpleader litigation.

Conflicts Between Employer Portals and Insurer Records

Many group life insurance plans rely on employer portals to process beneficiary updates. Disputes arise when the employer’s system reflects an updated beneficiary, but the insurer’s system does not.

This conflict may occur because the employer failed to transmit the update, used outdated forms, or relied on a platform the insurer later claims is not authoritative. When two systems show different beneficiaries, insurers often refuse to decide the issue themselves.

How Families Can Strengthen a Digital Beneficiary Claim

When a digital beneficiary change is challenged, documentation becomes critical. Helpful evidence includes portal screenshots, email confirmations, HR records, metadata logs if available, and statements from the policyholder confirming their intent.

Evidence showing consistent intent over time, such as messages, witness statements, or prior updates, can also support enforcement of the digital change.

Why These Disputes Are Becoming More Common

As insurers rely more heavily on automated systems, they also rely more on technical requirements. Small inconsistencies in metadata, submission timing, or form completion can be used to justify denial. To avoid liability, insurers often default to the older beneficiary designation and force families to litigate the issue.

Digital convenience has reduced paperwork, but it has increased the risk of technical denials. Families facing these disputes must be prepared to challenge arguments based on systems and process rather than the policyholder’s true wishes.